Ultra Clean Holdings (UCTT)·Q4 2025 Earnings Summary

Ultra Clean Beats Estimates, Guides Above Street as AI Ramp Accelerates

February 23, 2026 · by Fintool AI Agent

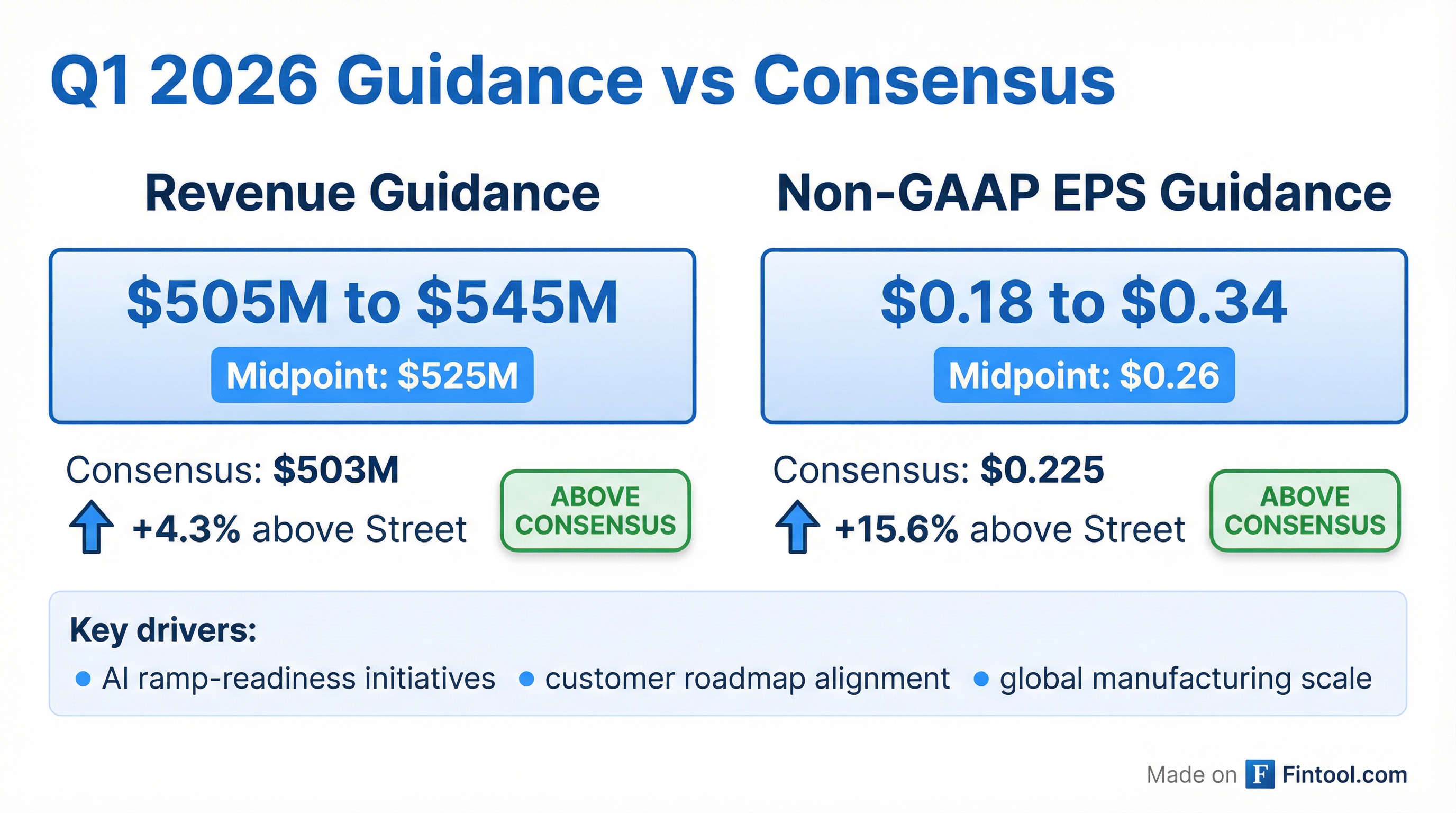

Ultra Clean Holdings (UCTT) delivered Q4 2025 results that edged past consensus, but the real story is the above-consensus Q1 2026 guidance signaling confidence in AI-driven semiconductor equipment demand. Revenue of $506.6 million and non-GAAP EPS of $0.24 both beat expectations, while Q1 guidance midpoints came in 4% and 16% above Street estimates on revenue and EPS, respectively .

The stock rose 3.8% to $61.41 during Monday's session—near its 52-week high of $61.64—before retreating 4.4% in after-hours trading to $58.70, suggesting investors are digesting whether the guidance justifies a stock that's rallied 255% from its 52-week low.

Did Ultra Clean Beat Earnings?

Ultra Clean delivered a narrow beat on both revenue and EPS for Q4 2025:

*Using company's new "As Adjusted" methodology excluding unrealized FX gains/losses .

The company also revised its non-GAAP methodology starting Q1 2026 to exclude unrealized foreign exchange gains and losses, which it believes provides "a more transparent and consistent measure of core operating performance" .

What Did Management Guide?

Q1 2026 guidance came in above consensus on both metrics—a notable signal given the company had previously cited "near-term volatility and reduced visibility":

The guidance midpoints suggest Q1 2026 revenue roughly flat sequentially while EPS expands, reflecting continued margin discipline and potentially a more favorable product mix.

What Changed From Last Quarter?

Several key shifts emerged in Q4 2025:

UCT 3.0 Strategy Launch: This was CEO James Xiao's first solo earnings call since taking the helm ~6 months ago. He introduced "UCT 3.0," a strategic transformation focused on ramp readiness, expanded NPX (new product introduction, development, and transition), and digital transformation with AI-compatible solutions .

WFE Outlook Upgraded: Management now sees 15%-20% WFE growth year-over-year, up from "low-to-mid teens" discussed at the Needham conference a month ago. James noted the forecast "increases week by week" .

$1 Trillion Semiconductor Market: Industry projections suggest the semiconductor market could reach $1 trillion in annual revenue by 2027—"possibly earlier"—significantly ahead of prior expectations .

Margin Recovery: Non-GAAP gross margin improved to 16.1% from 15.3% in Q2 2025, though still below the 17%+ levels seen in mid-2024 .

Goodwill Impairment Behind It: FY 2025 included a pre-tax, noncash goodwill impairment of $151.1 million, which drove the full-year GAAP net loss of $(181.2) million or $(4.00) per diluted share . This non-cash charge is now in the rearview mirror.

Non-GAAP Methodology Change: The company is excluding unrealized FX from non-GAAP results going forward, which it believes better reflects operational performance .

How Did the Stock React?

UCTT shares have been on a remarkable run, trading at levels that significantly exceed analyst price targets:

The after-hours weakness suggests the market may be questioning whether guidance, while above consensus, is enough to justify a stock trading 53% above Wall Street's average price target heading into the print.

What Did Management Say About AI?

CEO James Xiao framed the current environment as a structural shift, not a cyclical upturn:

"We're no longer preparing for a semiconductor recovery. We're entering a structural expansion of wafer fab equipment driven by AI infrastructure and physical AI demand... What we are witnessing is not a normal cyclical upturn, it is an AI technology inflection."

"The evolving AI roadmap, from Generative AI to Physical AI and Agentic AI, and ultimately artificial general intelligence, or AGI, is driving greater end customer confidence and accelerating investment in AI infrastructure."

On technology drivers, James highlighted the increasing complexity benefiting UCTT:

"Rising device complexity is accelerating wafer fab equipment spending as leading-edge fabs deploy new materials like molybdenum and new structures such as Gate-All-Around and high-bandwidth memory. These technologies require tight integrated solutions across deposition and removal, with increased depth etch CapEx intensity, which provide a tremendous growth opportunity for UCT."

The emphasis on "ramp-readiness" and customer roadmap alignment suggests UCTT is preparing for a multi-year semiconductor equipment expansion tied to AI infrastructure buildout—a more bullish stance than the "near-term volatility" language from prior quarters.

Q&A Highlights: What Analysts Asked

On 2026 Shape: Management expects a "step function" increase in the second half, with growth beginning in Q2 and accelerating through Q3 and Q4. "The run rate for September will be a very strong pickup from June, maybe a strong pickup again from September to December" .

On Outgrowing WFE: James expressed confidence UCTT will match or exceed WFE growth: "Because we have well-planned extra capacity that really can address $3 billion, we will capture more opportunities... We're pretty confident we will be on par with WFE growth or even higher" .

On Capacity and Utilization:

- Current utilization: 65% globally

- Current capacity: ~$3 billion in revenue

- Long-term target: $4 billion revenue run rate (requires only "modest incremental clean room investment")

- Asia capacity shifting from 50% to 60% to align with customer manufacturing footprint

On China Exposure: China OEM revenue is less than 7% of total revenue and expected to remain flattish in 2026. James noted: "I would not put too much emphasis on this" .

On Gross Margins: Q1 expected roughly flat to slightly up from Q4, with "sequential margin expansion in a meaningful way" expected in Q2, Q3, and Q4 as volumes increase .

On Memory Cycle: Management sees a multi-year upturn. Key points:

- Memory shortage could last until 2028 per customer feedback

- HBM is consuming DRAM capacity, requiring more WFE investment to address regular DRAM demand

- NAND upgrades from 2xx to 3xx and 4xx layers continuing

- Lam Research talking about "$40 billion over multiple years" of NAND upgrade investment

- AI-specific memory showing 2-3x CAGR versus regular memory market

On Services Growth: Expecting double-digit growth in 2026, also second-half weighted. Well-positioned for U.S. foundry logic ramp .

Segment Performance

Q4 2025 revenue breakdown by segment:

Services continues to carry significantly higher margins (29.7% non-GAAP vs. 14.1% for Products), though it represents just 12.7% of total revenue.

Full Year 2025 Performance

FY 2025 was challenging, marked by the goodwill impairment and margin compression:

The GAAP operating margin swing was driven primarily by the $151.1M goodwill impairment charge .

Balance Sheet Snapshot

The company generated $65.6M in operating cash flow for FY 2025, roughly flat with FY 2024's $65.0M .

Key Risks and Considerations

Valuation Disconnect: The stock trades significantly above analyst price targets after rallying 255%+ from its 52-week low. The after-hours pullback may signal concerns that guidance, while above consensus, doesn't justify current levels.

Margin Pressure: Non-GAAP gross margins remain ~100 bps below FY 2024 levels, and GAAP operating margins turned negative in FY 2025 (excluding the goodwill charge, operating income was still down materially YoY).

Customer Concentration: As a supplier to semiconductor equipment makers, UCTT's results are highly correlated with WFE (wafer fab equipment) spending cycles.

Tariff Exposure: Management previously noted tariff recovery mechanisms are in place for ~90% of tariffs, but trade policy remains a risk factor.

Forward Catalysts

- AI Infrastructure Buildout: UCTT is positioning for multi-year growth as hyperscalers and chip makers invest in AI compute capacity. Management sees the semiconductor market reaching $1 trillion by 2027

- WFE Upcycle: Management now expects 15%-20% WFE growth in 2026 and is confident UCTT can match or exceed that rate

- Memory Super-Cycle: Multi-year memory upturn with HBM, NAND upgrades, and AI-specific memory growing 2-3x faster than regular memory

- U.S. Foundry Ramp: Well-positioned for leading-edge foundry logic ramp in the U.S., expected to drive services growth

- Margin Expansion: Sequential margin improvement expected through 2026 as utilization rises from 65% toward capacity

- New COO: Robert Wunar was appointed as COO in January 2026, potentially signaling operational improvements ahead

The Bottom Line

Ultra Clean delivered a modest beat on Q4 2025 results, but the real message is in the above-consensus Q1 2026 guidance. Management's confidence in "ramp-readiness" and AI-driven demand suggests they see a clearer path to growth than the "reduced visibility" commentary from prior quarters implied.

The question for investors: Is the guidance strong enough to justify a stock near 52-week highs that's already priced in significant recovery? The after-hours pullback suggests the market isn't entirely convinced—at least not yet.

Related: UCTT Company Profile | Q4 2025 Earnings Call Transcript

Values marked with asterisk () retrieved from S&P Global.*